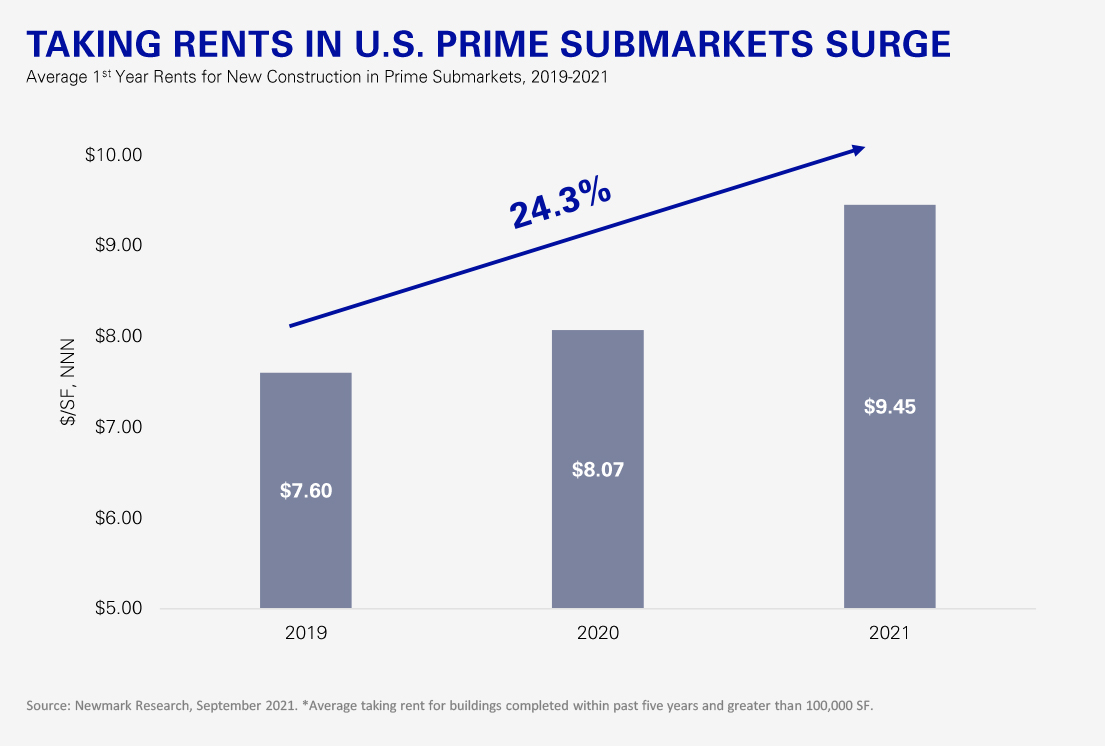

Rents for modern warehouse product are surging, a trend acutely felt in the most desirable logistics locations (“prime submarkets”) across the country. A prime submarket is often centrally located within a metropolitan area and offers access to critical infrastructure, including airports and seaports, major highways and rail lines – fundamental attributes for tenants focused on reducing transportation costs and transit time. Supply, especially modern product, is typically limited in prime submarkets, contributing to outsized rent growth for new construction. In at least six of the nation’s prime industrial submarkets, average taking rents for new construction are poised to cross the $10.00/SF mark – or have already crossed it. Since 2019, taking rents for new construction have increased by an average of 24.3% across prime submarkets, with some observing almost double that growth. The substantial savings on transportation costs achievable in these key locations allows occupiers to absorb escalating rents, which make up a smaller share of total operating costs. Given the combination of high rents and limited development, infill and redevelopment projects will become increasingly common in prime submarkets. Tenants that cannot find suitable space or are unable to pay elevated rents will continue to spill over into adjacent submarkets, helping to drive rent growth across market geographies.